Eminence Ricky Sandler Autodesk ADSK Lennar LEN Asbury ABG Dunkin Donuts DNKN Google CF CBRE CBG Zynga ZNGA Homebuilders Homebuilding AutoNation AN Group GPI Hedge

For some time now you've articulated three pillars to your investment strategy. Describe those and the basic rationale behind them.

Ricky Sandler: With all three pillars we're looking for shots on goal that will allow us to earn outsized returns. The first two, quality and value, haven't changed since we first spoke [VII, August 25, 2006]. The third, which revolves around investor perception, we formalized more than five years ago and believe has been very net positive for us.

When we talk about business quality, we're looking through our fundamental research to assess the company's ability to protect and grow intrinsic value. If the dollar of assets you buy is increasing in value at an above-average rate, that's an opportunity to generate alpha. Some of the analysis is numerical, like looking for high returns on capital or an ability to turn earnings into cash. We're also looking at industry structures and business models to judge the sustainability of those returns and, ideally, whether they're likely to improve. The emphasis is always on being prospective and not retrospective. One of the biggest dangers in value investing is falling for the formerly high-quality business that is getting slightly less high-quality every day. With all the disintermediation going on, that's a bigger risk today than ever.

Our value focus will be obvious to your readers. Paying 60 cents on the dollar for something increases the odds it will outperform the market over time. Here again our emphasis is on the future. We're looking for businesses that based on what we believe they can do over the next three years are statistically inexpensive. An Autodesk [ADSK], for example, which is going through a business-model transition and an operating overhaul, doesn't look inexpensive today. A Dunkin' Brands [DNKN], which we believe has an exemplary business and tremendous growth potential, doesn't look cheap today. On our expectations, however, we think both are terrific values.

ON INVESTOR PERCEPTION:

We can’t just hide behind the argument that eventually “value will win out.” We need to understand why and when.

Focusing on investor perception really comes from the realization that the investment business is one part having the right underlying philosophy, one part doing great research and analytical work, and one part a game, where you have to understand the mindset, psychology and emotions of people on the other side of the trade. So "investor perception" to us has two dimensions. The first is that we understand in detail the prevailing view on a particular company and its stock and that our view is differentiated in specific ways. The second is that we understand how and why that prevailing view is likely to change. I'm often asking, "What's the next guy's thesis?" Why is he going to buy it from us 18 months from now when the stock is up 50%? It's not just going to be that it's worth 50% more. It's important to imagine the narrative that will make the next investor think it's a good investment then.

Why did you think you had to add this element to your strategy?

RS: I'd argue that stocks today can stay more disconnected from intrinsic value for longer periods of time than was historically the case. Unfortunately, post financial crisis, there are fewer dyed-in-the-wool, active value investors who you can count on to step in and buy in volume with a long-term perspective – closing the value gap – when something gets really cheap. We're long-term investors, but we're not given the luxury to wait forever to be right. Three years is about all we have. We can't just hide behind the argument that eventually "value will win out." We need to have a much better sense of why it will win out and when.

People ask me if we would have done even better if we'd added this third pillar earlier, when it wasn't as critical. You never know, but I think we would have.

Before asking for an example or two where a focus on other investors' perceptions helped, how do you even judge what the "prevailing view" is?

RS: There's both an art and a science to it. Where there's detailed sell-side research, you can track pretty closely what you believe relative to analysts' views. If analysts look at a company on a non-GAAP basis, for example, even if we don't think that's legitimate we'll track our operating estimates on the same basis to see where our view differs. We'll research the big owners of the stock and can draw inferences from that. We look at short interest. We go to idea dinners and idea lunches. All these types of things can give us a fair read on investor perception and where we might be differentiated.

To give a classic example of how investor perception comes into our analysis, in 2012 there was concern with Google [GOOG] around how a shift to mobile advertising would be dilutive to the company's business. Costs-per-click were coming in lower for mobile ads, negating some of the upside from the growth in mobile overall. We did a lot of research around this and ultimately concluded that the shift to mobile would be much more positive than generally perceived. If you were searching with a mobile device, you were more likely to actually do something than if you were sitting at your desktop. This hadn't been proven out so advertisers weren't yet paying for it, but we expected both of those things to change. If we were right, investor sentiment would improve and the stock would re-rate. Even in such a big-cap name, the upside over the course of 18 months when that actually happened was fairly dramatic.

Has there been a similar dynamic with software companies transitioning from site licenses to cloud-based subscriptions, such as Autodesk?

RS: Absolutely. Investors get worried as earnings estimates keep coming down as you cycle out of big up-front licenses to lower-ticket annual subscriptions. Absent history, there's also considerable uncertainty over lifetime customer values and returns. If you recognize the positives before the market does – and again, if you're right – the upside can be quite attractive. Adobe Systems [ADBE] was a great positive example for us. We think Autodesk still is.

Has the way you go about things evolved at all due to the rise of passive investing?

RS: Assets under management in passive, quant and smart-beta strategies have gone from 17% of the market to 35% in the past several years. People like to say this is a fad, but investing by computer is here to stay and I think you make a mistake to bury your head in the sand and hope it all goes away.

If I tell you that investor perception is one of my pillars, I wouldn't be doing my job if I wasn't trying to understand the perception of the computer when it comes to my stocks. We have begun to focus on our internal capabilities to understand what that is. A lot of that is breaking down the factors that matter to quant investors. If I'm looking at a short or long that I think is mispriced, I also need to know what might trigger the quants to buy or sell. Estimate revisions are an important factor, so for my short to work out maybe I'm going to need to see forward estimate revisions come down by 5%. Volatility is a key factor. Nine-month price momentum is a key factor. And that's just covering the fact-based quants. You also have database quants who are taking in thousands of signals on everything from insider trading, to satellite imagery of parking lots, to credit-card data. These investors are moving stocks as well and we need to better understand how they work.

ON NEW COMPETITION:

I’m not doing my job if I’m not trying to understand the perception of the computer when it comes to my stocks.

I have yet to figure out if, or how much, we will actually change to really incorporate all this. It could help our judgment of investor perception. It could help prioritize ideas. If I'm looking at four stocks but two just started to screen negatively on a bunch of quant factors, maybe I'll prioritize the other two that don't have the same setup. It could impact execution. Maybe I love a stock but it's screening poorly on key factors, so I'll buy a 2% position now and wait until it's closer to the other side from a quant perspective before I take it to 4-5%.

We're still building our understanding and capabilities. It's possible we change very little, but I do know a couple things for certain. One, I can't ignore this because it's not going away. Two, we are bottom-up stock pickers at heart and that won't change in any material way. Those two fundamental beliefs combined with a lot of learning we have to do will inform how we think about this 12 to 18 months from now.

How would you characterize your idea pipeline today?

RS: Good. In general, as less and less money is managed based on micro, fundamental factors, that creates more opportunity for misperceptions and dislocations.

This has changed somewhat since the election, but one big anomaly we wrote about in our second-quarter letter was the valuation gap between stocks perceived to be low risk and stocks perceived to be high risk. Asset allocation into "safe" stocks as bond substitutes combined with the fact that most quantitative strategies have a healthy factor bias towards low volatility created significant valuation premiums for low-beta stocks. The quintile of stocks with the lowest beta traded around 20x forward earnings, a 50% premium to the quintile of stocks with the highest beta, which were at 13x earnings. Over the past 35 years, low-beta stocks typically traded at a 12% discount to high-beta stocks on forward earnings. That disconnect resulted in our finding much more value in good companies that have high betas and perhaps some perceived cyclical risk to earnings. That would include things like auto dealers and homebuilders, which we can discuss in more detail later.

Another important source of ideas are those situations where something is thought to be dead money for the next 12 to 18 months. Short-termism is always there, but we're finding it creating even more opportunity today. I'm generally not that active in commodity-based businesses, but one example we've found interesting recently is CF Industries [CF], the fertilizer company. We bought into this after management said on its second-quarter call that it expected the pricing environment in the industry to be bad through 2017. We understand that, but we also see an industry where demand growth is fairly stable, where CF is the low-cost producer, and where we believe it has a structural competitive advantage because of its sourcing reliance on low-cost U.S. natural gas. There's excess supply now, but the upper half of the cost curve is losing money on a cash basis. We think it's just a matter of time before supply comes down and prices increase. In that scenario if we can buy the guy at the low end of the cost curve at 30% of replacement cost, which was the case with CF, I like that framework.

What was going on in the industry or at the company that attracted your attention over the summer in commercial real-estate broker CBRE Group [CBG]?

RS: The stock had sold off from the high-$30s to mid-$20s primarily on cyclicality in the company's sales and leasing business. Fear that that piece of the business is topping out isn't totally wrong, but we think it's overstated given the impact on the overall business.

The institutional memory here is that when the cycle turns the company is in trouble. Going into the 2008 crisis the balance sheet was 3.5x levered and the sales business accounted for 30% of profits. As things fell apart the company had to do a very dilutive capital raise. Today leverage is down to one turn and the business mix has changed. Sales accounts for maybe 15% of profits today, while they've built up a fee-based, recurring-revenue facilities-management business that we estimate produces 35% of total profits. The overall mix is now much more stable.

We also think we're in the second inning of the global outsourcing of real-estate services. If a company owns and manages its own real estate, it's typically a non-core competency – not unlike IT – that can be outsourced to large, third-party providers with natural scale benefits. CBRE is the largest buyer of carpet in the world, for example. It can also bring tremendous expertise to managing real-estate properties at lower cost. All that allows customers to save money and outsourcers to still make a reasonable profit. CBRE is already the biggest player in the space by a lot, and we think this could be a ten-year, double-digit-growth asset. With the stock in the mid-$20s, we didn't think that upside was well reflected at all. [Note: CBRE shares now trade at just over $31.]

Is online-gaming company Zynga [ZNGA] a bit off the beaten path for you on the long side?

RS: This is something we've owned for a couple years and hasn't really done much, but we still look at it as an extremely long-dated call option on the company's ability to improve profitability and capitalize on its position in an attractive, fast-growing space. Cash and the building it owns in San Francisco are worth maybe 65% of the current market cap, so you're not paying much for core franchises such as Farmville, Words With Friends and Zynga Poker and Slots, which generate more than $700 million in annual revenue. If management gets anywhere near its 20% operating-margin goal and/or revamped game development can generate another winning franchise or two, we'd expect to see a significant revaluation of the stock.

ON FIELD RESEARCH:

In a world where communication is so tightly controlled, our own proprietary research is as important as ever.

You've always put a lot of emphasis on the field research Eminence does as a differentiating factor. Any updates on how you go about it?

RS: In a Reg-FD kind of world where communication with companies is so tightly controlled, our own proprietary research is as important as ever. There are two main parts to it. The first, which is early in the process, is making sure we understand how business is really done in the space. How do customers make purchase decisions? What's the differentiation between companies' products? Who, if anyone, has pricing power? What are the key secular trends? What's going on at competitors? To really understand all this you have to talk to people in the industry.

The second part later in the research process is more thesis-specific or tension-point-specific. Our basic thesis with Autodesk, for example, was that it was in the top-10% of the best businesses we've ever seen while being close to the bottom-10% of the worst financially managed companies we've ever seen. Understanding the former, especially in light of the latter, was all about field research. Talking to resellers and customers made clear the technological superiority of the products, how entrenched they were in customers' work flow and how the lead over the competition appeared to be widening. Talking to industry contacts and former employees helped us understand what about the culture led to margins that were half what they should be. This kind of insight from field research was critical to our having the conviction to put a stake in the ground at the company and even be willing to go active at the risk of locking ourselves up.

Do you still require analysts to write up a concise thesis of their work on a potential long or short?

RS: It's not uncommon given all the work that goes into building an investment case for an analyst to get buried in the detail. You've spent weeks building out a detailed model, reconciling the financial statements, talking to management, doing field research. Putting your thoughts down on paper forces you to organize and lay out the thesis in a succinct way. It's a very good discipline for surfacing what really matters.

Describe the long versus short makeup of your portfolio today.

RS: We currently hold around 50 longs – the highest-conviction of which each are between 5-10% of the portfolio – and a more diversified number of shorts, usually around 90 to 100. On a notional basis our net exposure today is in the high-30% range, but on a beta-adjusted basis it's around 65%.

One thing we're doing a bit differently on the short side over the past five years or so is using non-equity portfolio hedges along with our single-stock shorts. Today we have currency hedges based on our look-through geographic exposure and our judgment on where we don't want to take currency risk. We also have fixed-income hedges on European high-yield debt and on 10-year Japanese sovereign debt.

Shorting Japanese debt has been a bit of a disaster for some smart investors for many years. Describe your thought process there.

RS: I'd go so far as to say shorting Japanese debt is perhaps the single macro trade that has lost rational investors more money than any other position I can recall. We were never compelled to do it until last quarter. If central bankers lose control of long-term interest rates it would have a very significant negative impact on equities. As a hedge against that, what system is most likely to break first? Japan has used quantitative easing the longest and taken it and fiscal irresponsibility further than any other developed country. It has zero interest rates, with 270% debt to GDP and a negative 7% fiscal surplus. The timing is clearly hard to determine here, but by using options that expire in two years we were able to cheaply hedge against something bad happening over that time.

This is one of those things where in 20 years your kid is going to ask you, "Dad, when people were lending money to governments with awful credit at 0%, wasn't that the greatest short of all time?" And you might mumble about how it wasn't that easy, central banks were doing this and that, and it just wouldn't make sense. We concluded that if we can buy protection against the downside of all that in a low-cost way, we should.

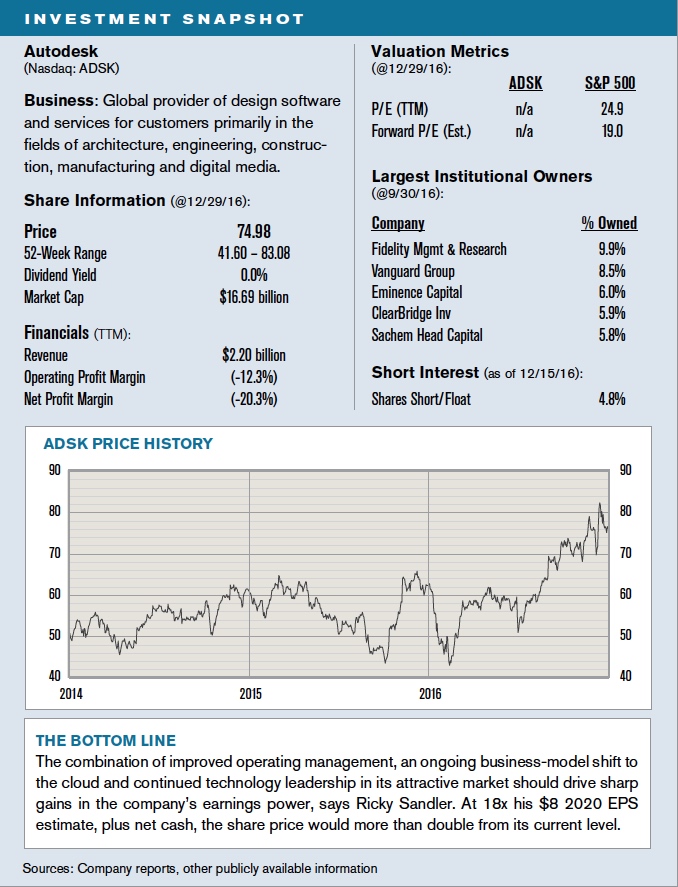

Returning to equity, describe the evolution of your large position in Autodesk.

RS: Late in the third quarter of 2015 we meaningfully increased our investment in Autodesk to approximately 10% of capital, with a plan to actively engage with management and the board in an effort to improve the company's financial performance. As I mentioned, despite very strong qualitative business characteristics, the financial and operating results fell far short of acceptable levels. We were convinced that with proper execution the company could earn significantly more money and generate significantly more cash than had been the case historically and than the market believed was possible in the future.

Pick a financial metric and it was likely worst in class. For example, looking at total cost of sale – including resellers and the direct sales force – many software companies run in the low-30% range of revenues, while Autodesk was in the low-50s. That's a massive difference and we thought it reflected the fact that resources were being misallocated, with too much money and human capital put behind products and markets unlikely to move the needle. They had hundreds of products, of which only a small subset really mattered and deserved significant resources.

We're pleased with the progress so far. Since our 13D filing the company has appointed three new directors, removed two directors, implemented a reduction in force, guided to no expense growth over the next five years, freed-up trapped offshore cash at no penalty, and upped its free-cash-flow guidance for 2019 from $4.25 per share to $6. We now think the path to realizing the potential we saw is smoother and the upside in the stock is larger as they deliver.

Talk more about what you like about the company's business.

RS: The core business is providing software used by architects, engineers and construction firms to design and manage building projects. That's for everything from remodeling your apartment to building MetLife Stadium or an electric power plant. In that ecosystem Autodesk has a dominant 70% market share, which is fairly natural for a business in which each user along the continuum from project start to finish pretty much needs to use the same software, which is what they were trained on in school.

There are a number of positive things going on in the business. Improved 3-D modeling makes it easier to see how a building sits in its natural environment and allows for better understanding of things like energy use and environmental impact. One result is that governments are increasingly mandating that projects are done using Autodesk software. There's also secular growth from the construction industry, a notoriously late adopter, investing more heavily in technology. You're starting to see iPads on construction sites. When you think about the money spent on construction and the savings involved if updating and approval processes were better automated and you could take days out of the schedule, software like Autodesk's is a real value add.

The company's push to a subscription-based cloud model has also been highly beneficial. It improves product functionality through things like better collaboration. It reduces the amount of piracy. It lowers the cost of entry for customers who are first starting to use the product. While the financials can look bad in the transition from up-front licenses to subscriptions, the lifetime value of the customer is materially higher with a cloud-based business and subscription model. I believe last quarter was the first one where all of Autodesk's products were available only by subscription.

The stock has done well over the past year. How are you looking at upside from today's $75 price?

RS: As the operating plan is executed we believe the company can deliver $8 per share in earnings by 2020. With an 18x multiple, plus net cash on the balance sheet, that would get us to more than $150 per share. We think that's conservative because it doesn't include the reasonable use of capital to buy back shares and assumes a multiple that is 15-20% below what high-quality software companies with recurring revenues typically earn.

ON ACTIVISM:

It’s become an easier tool to use. Management teams find it harder to ignore you and are more willing to listen.

Should we expect more activism from Eminence?

RS: Constructive shareholder engagement has always been something we've done. But given what has happened around shareholder activism it's now an easier tool to actually use. Management teams find it harder to ignore you, especially when it's not what you typically do, and they are much more willing to listen. That doesn't mean we should use it a lot – it's expensive, time consuming and you're less liquid. The bar is high but we'll pick and choose when and where it makes sense.

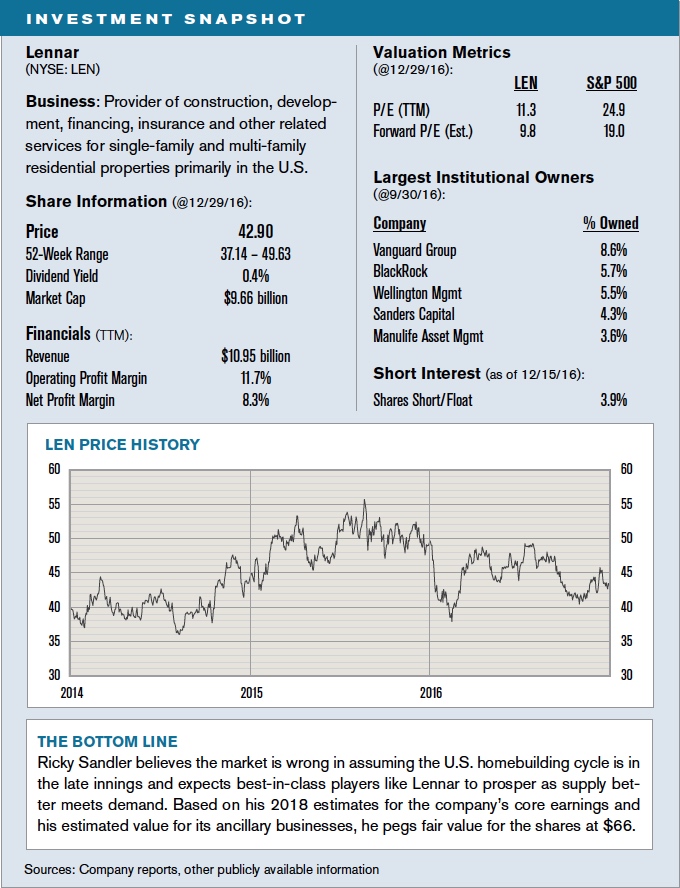

You have a long history investing in U.S. homebuilders and own more than one today. What's the general thesis behind that?

RS: I've covered this industry for 25 years and understand that it's generally a business more to rent than own. But sometimes the stocks get crazy cheap and reflect a misunderstanding of the cycle. Our position in it today is the biggest we've ever had and I would say it's the first time where I believe I can be an investor for several years.

The backdrop is this: we need to produce about 1.6 million homes in this country to meet demand for household formation, obsolescence and slight growth in second homes. That's single-family and multi-family homes, so we're not debating about whether people want to live in cities vs. the suburbs. We were above that production level in the bubble but for a decade now we've been either underbuilding or dramatically underbuilding. Even after a long recovery, today we're still under-producing that mid-cycle level by 20-25%. Obviously there's a lot of catching up to do.

So what's up? What's up is the millennials. They're the primary source of new housing demand but they're getting married and having kids later. Now the leading edge of millennials is just turning 35 and there's lots of data to support that they will start getting married and having kids and want a house of their own, regardless of whether they rent or buy. As that happens it's a very positive tailwind for homebuilders, particularly the bigger ones that have access to cheap capital and scale in production.

Despite that backdrop homebuilder stocks trade at prices suggesting we're very late cycle. Multiples are less than 10x earnings, as if earnings are about to cliff. They trade at 1.3x tangible book, versus a historical norm around 1.6x. The market seems to think we're in the eighth inning and we think we're in the second.

Why is Lennar [LEN] one of your top picks to benefit?

RS: Based on quantitative results over 30-plus years and our qualitative understanding of the industry, we consider Lennar the best company in the space with the best management. While it's an excellent operator positioned well by type of home and geographic exposure, capital allocation is the real differentiator, especially around land purchases and deploying capital into ancillary business ventures. They've invested approximately $1.2 billion into three businesses we're extremely excited about, a multifamily-construction business, an asset management/lender platform, and a strategic land developer predominantly in California. We believe all three of those businesses can be worth multiples of the capital currently deployed, but they are largely being ignored by investors due to the difficulty in assigning near-term value because they're not yet earning much of a return.

With some ups and downs, Lennar's shares have gone essentially nowhere in the past two years. How are you valuing them today at just under $43?

RS: Assuming continued modest recovery in the housing cycle – without the pent-up production deficit really being addressed, which we believe will eventually happen – we estimate 2018 earnings for the core housing business at just under $4.70 per share. On that we put a 12x multiple, which we consider reasonable if we're right about where we are in the cycle for the best company in the industry. That's $56 per share. The ancillary businesses, assuming they earn the returns we expect, we value at another $10 per share. That brings us to a $66 fair value.

What, as you say, is the next guy's thesis?

RS: The current investor is worried about interest rates going up. The current investor is also worried about some margin weakness, which makes him think the cycle is over rather than just that margins were abnormally high as some of the very cheap land builders bought in the crisis got monetized. The next guy is going to be talking about the massive production deficit correcting and millennials moving into homes, and he's probably going to pay more than 12x earnings. Given the accumulated production deficit we could be way above trend line for years.

You own multiple auto dealers – Asbury Automotive [ABG], AutoNation [AN] and Group 1 Automotive [GPI] – where the prevailing view is also that the relevant cycle is in the late innings. Describe your bullish case there.

RS: On the surface this looks like a fairly low-margin business that's highly cyclical and where the seasonally adjusted annual rate [SAAR] of car sales in the U.S. has peaked. Not great.

Our basic case rests on the belief that while SAAR may not grow much from here near-term, it isn't in for a material decline and, if that's the case, car dealers can increase earnings at healthy rates because of both secular and cyclical growth in their parts-and-service businesses. That business accounts for only 15-20% of revenue but more than 50% of gross profits and two-thirds of EBIT. With all the attention paid to new-car sales, we think that's overlooked.

The secular growth in service comes from the increasing complexity of cars, which translates into people using the dealer rather than an independent service provider. It's also driven by car brands pushing extended-service plans and certified-pre-owned programs that are meant to strengthen the brands and also tend to promote more servicing done at the dealer.

The cyclical element is a function of car buyers in the first seven years of ownership being more likely to use the dealer for service than an independent repair shop. Given the depression in new-car sales in 2010, 2011 and into 2012, from here you're going to see growth in the zero-to-seven-year-old car base as the depressed years roll off. Overall, we expect dealer parts and service volume to grow 6-12% annually over the medium term and profits on that business to grow closer to 20% per year.

Are you worried at all about disintermediation eventually from autonomous-driving cars and vehicle sharing?

RS: First of all, we don't expect disintermediation of the service business. Second, at 8-10x current-year earnings we don't think valuations reflect the durability and growth we forecast in earnings and are at levels that more than compensate us for very long-term technology-related risks.

To get a sense of the upside you see, walk through your valuation of Asbury's stock, now trading at just under $62.

RS: Asbury is a best-in-class competitor as measured by returns on capital, margins and capital allocation, in a market where all the big players have more or less diversified geographic footprints and nameplate exposure. Based on our 2017 EPS estimate of $6.90, the shares trade at a 9x P/E. On our $7.95 number for 2018 the P/E is only 7.8x.

We believe by the end of next year Asbury can trade at 13x forward EPS, which gives us a price target of $103. These companies have never gotten market multiples, but if you actually look at how they performed in the recession the business is more resilient than I think it gets credit for. As parts and service becomes even more important, there's a good case for the stocks to be re-rated.

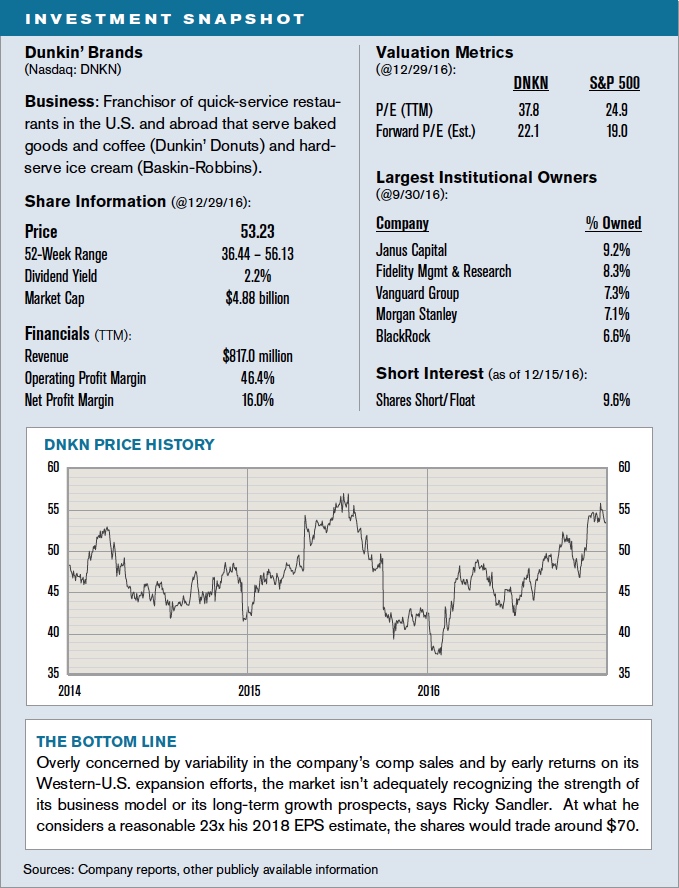

Explain your ongoing enthusiasm for Dunkin' Brands.

RS: It's a great business growing with other people's capital. Roughly 90% of its profit comes from franchising the Dunkin' Donuts brand, which is more of a coffee business than a food business with 65-70% of revenues coming from beverages. Returns on capital to franchisees are strong, representing the power of the brand.

The company also has tremendous opportunity to grow. It has 7,500 stores east of the Mississippi, but only 500 west of the Mississippi and very little internationally. The potential to double units in the U.S. is real and visible and it's reasonable to assume they could double that base again through growth outside the U.S.

Investor perception has gotten a bit better, but when we were buying in the third quarter there was concern over some volatility in comp sales and traffic levels. There has also been worry over franchisee returns on the West Coast coming in well below the sky-high levels generally earned in the East.

With respect to comps, the company was rolling out some important new products and technology initiatives which may have caused short-term variability but which we expect to be positive over the long term. We also think the worry over West-Coast returns is short-sighted. Year-one returns – which is much of what you're seeing from the West Coast – are inevitably lower because coffee starts out at maybe 35% of the product mix, before increasing as the brand gains relevance and customers build store visits into their routines. The parent company has also tried to improve the franchise effort in the West by bringing in experienced partners from the East Coast and by reducing investment costs for franchisees through developing more local supply chains and making the store layouts more efficient. We've done a lot of field research around the growth potential and execution in the West and are confident the opportunity is as good as we originally thought.

One other thing I'd mention is the company's entry into the ready-to-drink coffee business in partnership with Coca-Cola. This area – think frappuccino out of the fridge – is dominated by Starbucks but we think Dunkin can earn the same type of relative share it already has in ground coffee and K-cups, where it competes very well. Most analysts don't seem to be paying attention to this, but we think this alone could add 25 cents per share to earnings in the next two years.

What do you think the shares, now at $53.25 and near an all-time high, are more reasonably worth?

RS: We see annual earnings growth of 15%-plus for some time, driven by 5% unit growth, low-single-digit comp growth, operating leverage and use of excess cash flow to return capital to shareholders. At our target 23x multiple on $3 per share in estimated 2018 EPS, that gets us to a share price of around $70. That's more than 30% upside from today's price, including dividends.

We think the downside is low based on the defensibility of the cash-flow stream and the strategic nature of the asset. If there's any stretch of sustained underperformance we wouldn't at all be surprised to see a strategic buyer or activist investor get involved. That adds to the investment appeal and also helps control our downside risk.

What's your take on the post-election market rally?

RS: First of all, some of it reflects the fact that earnings were set to grow for the first time in two years right about now anyway, as many companies cycled past oil-related issues and currency-related issues. At the same time, the new narrative around tax cuts, fiscal stimulus and less regulation is really the first positive narrative – other than, "Where else am I going to put my money?" – in a long time. That translates into both management confidence and investor confidence.

The big medium-term risks are still there, like the threat of the European Union breaking up, central banks losing control of interest rates and China deleveraging. But I could argue that while valuations aren't cheap they aren't a problem either, and that while investor sentiment is better it's not overdone. I could see the rally continuing into next year. Of course before you get too deep into the year the rubber is going to start meeting the road on things like fiscal policy, tax policy and trade policy. The new administration is going to have to actually succeed in getting things done for the expectations to meet the reality.

On the subject of expectations meeting reality, why do you think hedge funds in general have had such a tough time of it?

RS: It's relatively simple. Since the financial crisis the average hedge fund has had too-low returns and too-high fees. If you're sitting on an investment committee you look at that and you're right to question what's going on. That's not at all to say good hedge funds aren't worth their fees, they are, but there's going to continue to be a weeding out.

Why do you think general hedge-fund performance has been poor?

RS: I'd say one big culprit has been increased pressure to not lose money. Hedge funds generally did a lot better than the market in 2008 and while some investors saw that as a job well done, a lot were livid. I think the pressure to not lose money since then has created these episodic periods of everyone de-risking at the same time. The most expensive form of risk management is to decide you need to cut risk because your portfolio's down. The horse is already out – cutting risk then doesn't do anything but lock in losses.

I think the crowding issue is also real. That can be a negative because managers may find their view isn't as differentiated as they thought. It's also a negative when that crowding results in increased volatility as people go risk-on and risk-off. Quants tend to underweight those types of crowded positions because they look more volatile. That helps stretch out how long it takes for any gap between price and value to close.

In 2011 we started a long-only fund that was opened to investors about a year later and essentially replicates the longs of our hedge fund. I think these can be very attractive products both for managers and for investors. It's been great for us. It's a business stabilizer and now makes up about one-quarter of our assets.

You started young but have been at this for quite a while and probably don't need to do it anymore. Any thoughts about slowing down?

RS: No. One reason is I'm a very competitive person and I want to win. But I don't view winning as making the most money and having the most toys, although I have my share of those. I view it as building a lifetime track record and ultimately being perceived as a great investor – you have to do it well for a long period of time for that to happen.

I also still love the intellectual challenge of understanding companies and industries, of figuring out what something is worth, of playing the psychological game well. It's amazing how different things are from when I started in this business. It's not harder, it's different. All that continues to drive me and our entire team.