Tucker Golden Solas Natural Resource NRP NFI McCormick MKC Bluelinx BXC AdvanSix ASIX SWK SWKH Quantum QTM Amerco UHAL Public Storage PSA Coal Contura Alpha Ciner CINR REV REVG HHGregg New York NWY

You've been a committed long/short investor, through thick and thin, since starting your firm in 2004. Start out by describing your basic rationale for that approach.

Tucker Golden: We're confident we can perform over time in security selection and less confident we can do so in terms of things like market timing, sector rotation, geography, commodity cycles, foreign exchange and interest rates. By running the fund with low net exposure – today we're about 10% net long and on a beta-adjusted basis essentially market neutral – we try to isolate out the exogenous factors on which we don't want to bet and make very deliberate bets through stock selection.

Running a short book is valuable in other ways. Hedging out unwanted exposures in any idea allows us to have larger exposures in our best long ideas. Shorting also allows us to stay in the game when there is a market dislocation. Of course, we haven't had one of those for quite some time, but as I learned in 2008, and at a prior firm in 2002, a low-net strategy allow us to be on offense when other investors are thinking about liquidity and damage control, which should allow us to really shine coming out of those times.

In theory, and in practice, shorting keeps our outlook pretty cynical. Running through accounting screens every day at lunch, for example, is a good way to identify short ideas, but also helpful in catching things in potential longs we might otherwise overlook. I'd argue skepticism is a pretty valuable trait for any investor.

What type of situations attract your attention on the long side?

TG: We look for situations in which non-economic sellers create mispricings that should correct over time based on fundamental value. That could mean something as straightforward as time arbitrage, where there might be an overhang on a stock that could persist for two to three years and the average investor or the institutional analyst on a 12-month rotation schedule isn't very interested. If the stock today reflects that sort of apathy and we think the IRR is worth the wait, that can tilt the tables in our favor.

ON IDEA GENERATION:

We look for situations in which non-economic sellers create mispricings that should correct over time.

We also find ideas around spinoffs, carve-outs, rights offerings and post-reorgs, many of which involve the shareholder base turning over. We own a stake in Bluelinx Holdings [BXC], for example, which is a U.S. distributor of homebuilding supplies. Last October after 13 years as the 50%-plus controlling shareholder, Cerberus Capital decided to sell its stake through an underwritten offering at $7 per share. We already owned shares, based on a positive view that the company was turning around, that it might benefit from a reversion to the mean for single-family housing starts, and most importantly, that it had underlying real estate worth north of $20 per share, net of all liabilities.

The stock took a hit on the news that Cerberus was selling, at a point where we thought Bluelinx was on the cusp of real success. But peeling the layers back, you saw that Cerberus's fund that held the stake was two years past its shelf life and that, given the other deals the same people were working on, they just had bigger fish to fry. We saw a classic non-economic seller whose motives were temporarily different than ours and we added to our stake at the $7 offering price. Since then the business and balance sheet have continued to improve, the company completed a highly accretive merger in March, and we now believe it can earn $8 per share in annual free cash flow. The stock today trades around $36 and we still own it.

A past spinoff example that worked well for us was AdvanSix [ASIX], a chemical manufacturer spun off from Honeywell in 2016. In general we've found good opportunity in spinoffs that have very different characteristics from the parent with respect to size, liquidity and dividend policy, which tends to amplify the turnover in the shareholder base. AdvanSix was less than 1% the size of Honeywell, was in a cyclical business that was at a low point in the cycle and had no sell-side coverage. Within two weeks the entire shareholder base turned over, pushing the share price from a high above $20 to a low near $14. We concluded there was good management with good incentives and a decent business that was mispriced at what we thought was 3x normalized EBITDA. This one has played out and we ended up selling out north of $40 per share. [Note: ASIX shares currently trade at $33.50.]

Do you tilt at all toward smaller caps to find mispricing?

TG: I've come to the conclusion that small caps aren't necessarily as underfollowed as many might think. Often the research and analytical work done on small and micro caps is better because it's more authentic and original, start to finish, without crutches from sell-side research or companies making conference appearances.

That said, given the greater marginal impact of incremental buyers and sellers on price, you're still more likely to find mispricing in small companies. One current favorite is SWK Holdings [SWKH], a healthcare royalty finance company with a growing franchise and a stock trading at $10 against a book value north of $16 and earnings power of $1.30. We think the opportunity exists because the market cap is small, around $130 million, and because the stock trades over the counter due to the company electing not to meet the exchanges' independent-director qualifications. We think the discount shrinks quickly if they list on a major exchange, and in the meantime at this price and with the quality of their investment portfolio our downside risk is very low.

We're also paying attention on the long side to companies removed from leading indices, which sometimes can have a cap-size component. This has hair on it, but we established a position in Quantum Corp. [QTM] when the stock went from $3 to $2 after the company was deleted in June from the Russell 2000 index. The company's tape-storage business is secularly challenged, top management has turned over frequently, and there's an SEC investigation surrounding revenue recognition that has resulted in financial statements not being released since September 2017.

Through all that we've concluded that tape storage is quite viable in serving target media, entertainment and security markets and that the company has royalty and services income that is more stable and lucrative than the market seems to believe. Combined with cost-cutting opportunities, we think the company may ultimately earn over 65 cents per share in free cash flow, including benefits from net operating loss carryforwards. That made us pretty excited to buy stock at $2. The opportunity isn't there just because it's small and nobody cares, but that's part of it.

You mentioned looking at accounting screens over lunch for short ideas. Explain what you're looking for.

TG: First I'd point out a few things generally about our shorts. We gravitate toward ideas that aren't as crowded as your typical fads, frauds and failures. When highly shorted stocks that everyone expects to fail don't fail, they can go up far and fast. We also tend toward more mature companies, where timing isn't so important because they aren't growing rapidly. Finally, because they have infinite downside, we size our short positions accordingly, keeping them at 1-3% at cost, while we'll go up to 8% or so on the long side.

ON FINDING SHORTS:

We see more instances where earnings seem stretched. Our accounting screens have been quite productive.

We've had luck using accounting-driven screens to identify good, uncrowded shorts. We focus on material unexpected or hard-to-explain changes in accounting metrics that involve estimation or opinion. The most obvious examples would be shifts in accrued or prepaid expenses as a percentage of sales. There may be rational explanations, but when the changes don't make sense and improve reported profits, it might be worth further inquiry.

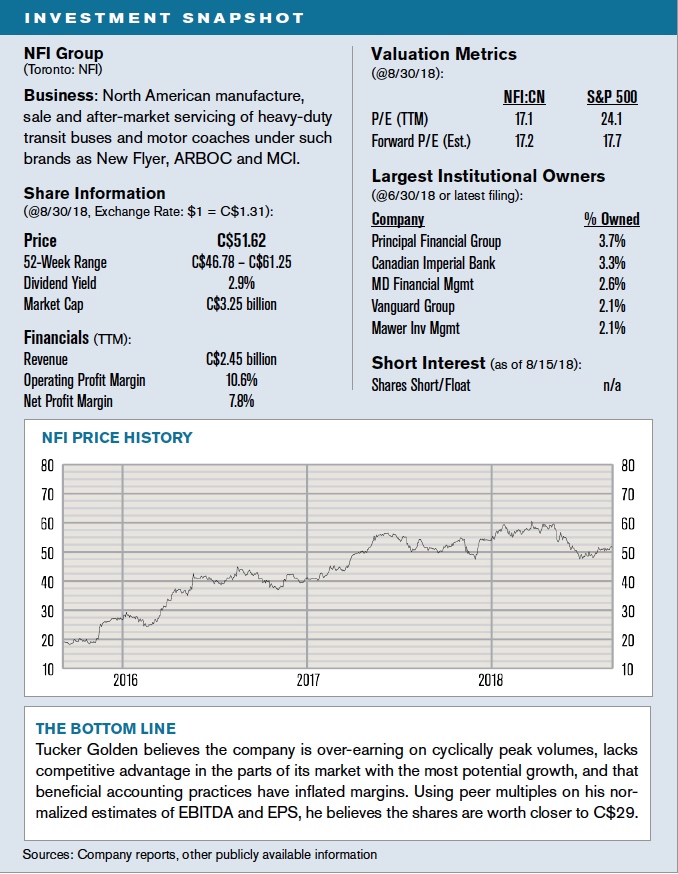

One of the things that got us more interested in bus manufacturer NFI Group [NFI:CN] as a short was the fact that gross margins seemed to be improving in a way that didn't make sense given the competitive backdrop. As we looked more closely we decided it had more to do with beneficial accounting – through increases in prepaid expenses and decreases in accrued expenses – than the real business.

We believe managers are under increased pressure in an environment like today's to make and beat guidance and estimates, so we're seeing more instances where it seems earnings are stretched and balance-sheet driven. Our accounting screens lately have been quite productive.

Your fundamental research often includes a "scuttlebutt" component. Why do you think that's important?

TG: Taking nothing away from the importance of financial modeling and analysis, you can gain only so much from living inside your spreadsheet. To get the understanding of the business you need to have conviction in your thesis, very often you have to go deeper, almost like an investigative reporter.

One of the ways we came to originally like Amerco [UHAL], the parent company of U-Haul, was understanding how they set up and maintained their deep network of rental pick-up and return sites, which many times are gas stations or storage facilities with extra space to accommodate U-Haul's business. We came to the conclusion that their network was a sustainable competitive advantage, requiring little capital beyond the trucks, but held together through aligned incentives and some pretty sophisticated technology. We wouldn't have gained conviction without making hundreds of calls to eventually talk to enough people to understand why dealers strongly prefer U-Haul.

With respect to Quantum, which I mentioned earlier, the best way to determine the extent of the secular challenge to tape storage was to talk to a lot of customers who used it. We came away from that believing that in many archival applications tape storage remains the most cost-effective alternative by a wide margin and that the secular-decline fears priced into the stock were likely overdone. Again, we couldn't have seen that staring at the financials or talking to other investors.

This type of research takes time, but we'd rather devote the time to that than modeling out every quarter to the penny in terms of EPS projections. I would say also that it makes the job more fulfilling. Interacting with people outside of your industry, creating new relationships, learning new things – that's all part of the fun.

To digress a bit on Amerco, are you keen on the self-storage side of its business?

TG: No. The market for self-storage has grown rapidly, but we worry that easy access to capital has driven excess supply. We like the interstate truck-rental business and think we're paying 5x EBITDA and 10x earnings for it on our view of normalized earnings. We're hedging our exposure to self-storage by shorting the biggest player in that business, Public Storage [PSA], which trades around 22x EBITDA on what we believe may be peak earnings.

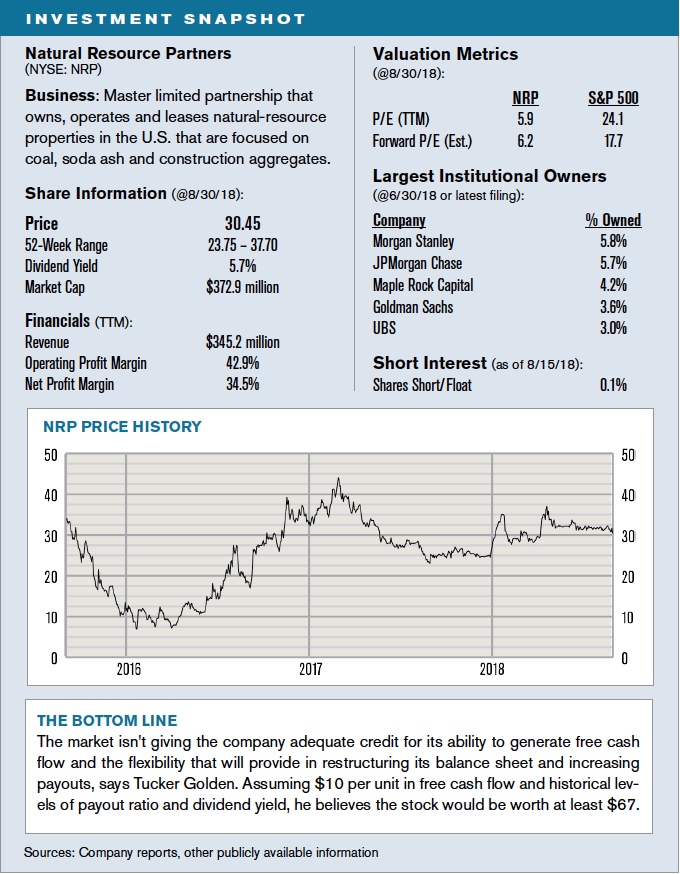

Walk through the broader investment case for one of your current long positions, Natural Resource Partners [NRP].

TG: The company is structured as a master limited partnership and operates coal-royalty, soda-ash and construction-aggregates businesses. The royalty business is the most important, generating roughly 70% of EBITDA, and consists primarily of leasing coal properties to producers in the business like Alpha Natural Resources and Contura Energy. It has coal price and volume exposure – two-thirds of which is to metallurgical coal – but the earnings profile is more stable than that of a coal producer, as most of the leases have protections in the form of minimum royalties. NRP also doesn't have direct exposure to pension and environmental liabilities, or to big capital-spending obligations.

The company's market cap has declined by close to 90% since early 2011, as declining coal prices put pressure on earnings and then management decided to drastically cut the distribution to unitholders in 2015 to focus on de-levering. Our basic thesis today is that the market isn't recognizing NRP's current and prospective free cash flow generation because it hasn't yet led to distribution increases.

Why hasn't it led to distribution increases?

TG: The company is generating free cash flow in excess of $10 per unit, which implies a levered free-cash-flow yield in excess of 30% on today's share price. So the potential to increase the distribution is there, but they've been disciplined in directing free cash to reduce leverage until they get net debt to EBITDA to around 3x, from an already decreased 3.5x at the end of the second quarter. Once they get there, which we expect to happen early next year, we expect management to either significantly increase the distribution, or potentially also hoard cash with a view to redeeming potentially dilutive convertible preferred securities issued at the bottom.

Are you hedging out the coal price exposure here in some way?

TG: Not at the moment. We generally don't short commodities or indices against producers, and the shares of a lot of producers are still quite cheap, so we haven't been able to construct a good hedge. In general, met-coal prices – which are the most volatile – have recovered from their 2015-2016 lows, and management has provided sensitivity guidance indicating that they could cover the current distribution by over 3x even if seaborne met-coal prices reverted back to 2015-2016 levels. The lack of a viable hedge has kept us from having as big a position as we might otherwise, but the risk/reward is attractive enough that we're comfortable with the coal-price exposure for now.

Are the non-coal parts of the business important to your thesis in any way?

TG: We don't believe the market is correctly valuing the cash-flow stream from the soda-ash operation, which consists of NRP's minority (49%) interest in the CinerWyoming JV, which is a trona mining and soda-ash refining operation controlled by publicly traded Ciner Resources [CINR]. We think there's an opportunity for NRP's management to close that valuation gap by selling their interest in CinerWyoming, and we believe the parent, Ciner Resources, would be a ready buyer.

How are you looking at NRP's valuation from today's $30.50 price?

TG: Over time, we would expect NRP's payout ratio to eventually return to historical averages. Assuming the company continues to generate free cash flow of approximately $10 per unit and targets a payout ratio of 60%-70%, that would imply a distribution per unit of $6 to $7. At a dividend yield of 7% to 9% – versus the long-term historical average of 7.5% – that would imply a price per unit of $67 at the low end and closer to $100 at the high end.

You mentioned earlier how NFI Group got on your radar screen. Explain why you're bearish on its prospects.

TG: The company is the largest transit-bus and motor-coach manufacturer in North America. Transit buses sold primarily to U.S. and Canadian municipalities account for roughly 70% of total revenues, while the balance of the business comes from motor-coach sales to intercity bus lines like Greyhound or Peter Pan.

There are a number of things we believe are working against the company. The transit-bus market has been surprisingly healthy, which we think has been driven more by increased visibility into federal funding for bus purchases – through what's called the FAST Act – than by true market demand. In fact, overall bus ridership is in secular decline, which appears to have accelerated recently. That tends to create a self-reinforcing cycle, where lower ridership leads to a cutback in routes and service, which further reduces ridership. Although we aren't counting on this, if autonomous vehicles and ride-sharing start getting traction, that could further reduce future transit-bus demand.

NFI has also been losing market share in transit buses since 2014 due to competitive pressures from both existing and new players. Volvo, the #3 player in the market, has been aggressively cutting prices to gain market share. El Dorado, owned by REV Group [REVG], has had success in increasingly pursuing the types of larger-municipality contracts in which NFI has been most active. In the electric-bus category, NFI is seeing significantly increased capacity from China's BYD, which is partially owned by Berkshire Hathaway, and from Proterra, which is run by a number of former Tesla executives and recently raised additional capital to continue to fund its expansion.

As I said earlier, we're leery of the fact that the company's peak margins in recent years, which we wouldn't expect given increased competition in the market, appear driven more by beneficial accounting than anything else. Accrued expenses have declined as a percentage of sales in amounts accounting for almost the entire recent improvement in gross margins, and we haven't found a reasonable explanation for the change.

What do you believe the shares, at a recent C$51.60, are more reasonably worth?

TG: The consensus view on NFI – six of the seven Canadian banks that follow it have rated it a "buy" – is that the company is the clear leader in an oligopoly, where its size and scale should allow it to compound as it expands outside of heavy-duty transit buses. We, on the other hand, think it's over-earning on cyclically peak transit-bus volumes, that it's not as competitively advantaged in the parts of the market with the most potential growth, and that beneficial accounting practices have inflated margins.

We estimate normalized EBITDA at C$284 million and normalized earnings per share at C$2.14. That compares with trailing-12-month levels of C$422 million in EBITDA and C$3.62 in EPS. On our estimates, at multiples in-line with peers of 14x earnings and 9x EV/EBITDA, we believe the shares are worth closer to C$29 per share, or about 45% below the current price.

Have you calculated a downside scenario?

TG: If peak volumes continue and the stock trades at a premium to peers – 18x earnings and 11.5x EV/EBITDA – the shares would trade around C$58. We don't ascribe a high probability to that scenario relative to our base case, so the risk/reward appears quite attractive.

Turning to another short, describe the downside you see in spice maker McCormick & Co. [MKC].

TG: McCormick is the #1 U.S. player in spices and seasonings, with a roughly 40% market share. Management used to include a chart in their earnings presentations showing the company's market-share trends in branded spices and seasonings, but that ended in Q3 2016 and we believe the brand's market share has fallen in each quarter since. The primary reason is the rise of better-quality and more highly promoted private-label brands. As that continues, the company's efforts to raise its spices' prices as an offset will become increasingly difficult.

A second key component to our bear case is that we believe McCormick vastly overpaid last year to acquire Reckitt Benckiser's RB Foods business, which included the French's mustard and Frank's RedHot hot sauce brands. The purchase price was $4.2 billion, approximately 19.5x EBITDA and 7.2x sales, for a company whose margins were already much higher than McCormick's, likely limiting potential cost synergies. Even worse, RB Foods started showing signs of weakness shortly after the acquisition was announced, with organic growth turning negative. That's likely the result of Heinz taking on French's in mustard and just a raft of new competitors in hot sauce, which strikes us as the kind of market where novelty is highly valued, making it hard for any brand to dominate for long.

What do you think the market is missing?

TG: The short interest is picking up, which makes us a bit nervous, but the general consensus seems to be that the company has been a pretty solid grower – at least in comparison to comparable companies – and that management will be as good as they say in integrating the acquisition and driving both revenue and cost synergies. We don't agree and think results below expectations will take the air out of what is now a premium-priced stock at all-time highs of 3.9x enterprise value to sales, 19x EV/EBITDA and 25x levered earnings on consensus 2018 estimates.

With the shares at $123.70, what valuation do you consider more appropriate?

TG: Using peer EV/EBITDA and EV/Sales multiples of 12.5x and 2.5x, respectively, on consensus 2018 estimates, we arrive at a fair value for the shares of $66 to $70.

One thing I'd add is that the company's margin for error has decreased post the RB Foods purchase, as it took on significant additional debt to do the deal. Net debt to EBITDA today is around 4.5x, vs. around 2x prior to the acquisition.

Talk generally about your discipline when it comes to selling.

TG: Our selling is always with a target price in mind, but we've vacillated over time on how close we let ourselves get to that target price before selling. We started out thinking we shouldn't be greedy and hold out for the last dollar. Then we thought if we're doing good work, it's OK to be a little greedy so as not to miss out on upside beyond our conservative assumptions. The current evolution is that if we're doing our best work, even in a challenging environment for value like we've had, your pipeline should be full of opportunities. There should always be something better than an idea that's 90% of the way there. We may still be building conviction in that new idea, but if we're pretty far into it and still think it's a 50-cent dollar, we should own more of that, and less of whatever we think we know inside out that may be at 90 cents on the dollar.

We're more diversified than usual right now on the long side, reflecting the fact that our long ideas with the most attractive risk/reward profiles have at the margin somewhat less downside protection than we usually like. It sounds and feels like we're stretching at times, but we've concluded that the prices in such circumstances more than compensate for the incremental risks. To better accommodate those kinds of ideas, we're limiting more than usual the capital exposed to any one of them.

ON MISTAKES:

It sounds lazy to say, "You win some and you lose some," but we think that's important to remember.

Describe an investment mistake you've made and any lessons learned from it.

TG: One of our worst investments ever was betting on the turnaround of home-appliance and consumer-electronics retailer HHGregg. There were clear industry headwinds, in particular with consumer-electronics spending migrating online, but we thought there were sound plans to mitigate the decline and that the value of the $1 billion appliances business far exceeded the sub-$100-million enterprise value. We thought the balance sheet was sufficiently strong and that the management team and board of directors were competent and had interests fully aligned with ours.

It didn't work out, to say the least. The company tried to fix everything at once, execution wasn't perfect, results deteriorated quickly, vendors panicked and liquidity dried up. We knew the scenario that played out was possible, but we ascribed too low a probability to it. If anything, the lesson was around position sizing. We averaged down along the way thinking they'd figure it out, which obviously backfired as the vendor and creditor psychology shift that took hold put the company under.

One thing I've learned is that you can't afford to be paralyzed by perceived mistakes or adverse outcomes. We're here to take calculated risks over and over with the expectation that, in aggregate, they will collectively result in significant reward. As much as I hate losing money, I don't want the fact we've done so at times to push us toward only boring and undifferentiated ideas that are going to keep us from achieving our goals of significant outperformance by longs and shorts.

If there's something to learn, we adapt and evolve and then get back to work. We could have come out of our HHGregg experience saying we're no longer going to look at retail turnarounds, especially in the age of Amazon. That would be the path of least resistance, but I think it's generally the wrong mentality for our business and results in mediocrity. In retail we've since seen promising turnaround potential in New York & Co. [NWY], a moderately priced women's apparel retailer. The setup for it was not dissimilar to HHGregg, but the outcome has been very different. We purchased the stock in 2016 at an average price of $2.16 and recently exited at an average price of $4.28, nearly doubling our investment in two years. It sounds lazy to say, "You win some and you lose some," but as long as your research and analytical process is anything but lazy, we think that's important to remember.

It's been dangerous for value investors to opine on overall market direction in recent years. Can we get you to take a shot at it?

TG: Given our consistently low net exposure, we don't have to have an opinion. But we've thought for several years now that we must be approaching some sort of reckoning, and we've been wrong. The good news is that we're still finding very interesting pockets of opportunity on the long side – it just requires more digging.

I'd put it this way: Right now I'm happier than I have been on average to be personally highly exposed to a strategy with little to no real market exposure. If we have a sharp correction in the market, we should be well situated and in a position to be offensive when opportunities on the long side are most compelling.