Small-cap investors pride themselves on finding off-the-beaten-path ideas that through the market’s neglect or disinterest appear misunderstood and mispriced. That describes well what Nitin Sacheti, portfolio manager of Papyrus Capital Management, sees in General Communication Inc., Alaska’s only cable-services provider. “You could say this is off the beaten path both literally and figuratively,” he says.

The remoteness and size of GCI’s addressable market is both a curse and a blessing for the company. Alaska's economy has stalled at the moment due to lower oil prices and stagnant population growth, but the lack of competitive interest in the market has allowed the company to establish a dominant position. It offers cable services to 98% of the state's population and its infrastructure for high-speed broadband access leaves that of primary fixed-line competitor Alaska Communications in the dust. The incumbent telephone utility, ACS offers only one plan for $80 per month, with speeds dependent on how far away customers are from its facilities. As a result, some 50% of its customers receive speeds of only 10 megabits per second. GCI offers 50-mbps broadband service at $60 per month, and 100-mbps service for $85.

On the wireless side, AT&T is the only major competitor but it lacks competitive coverage in rural areas and prices its packages at a roughly 20% premium to GCI. GCI is the only company in the state able to bundle cable, data, landline and wireless services, significantly reducing customer churn.

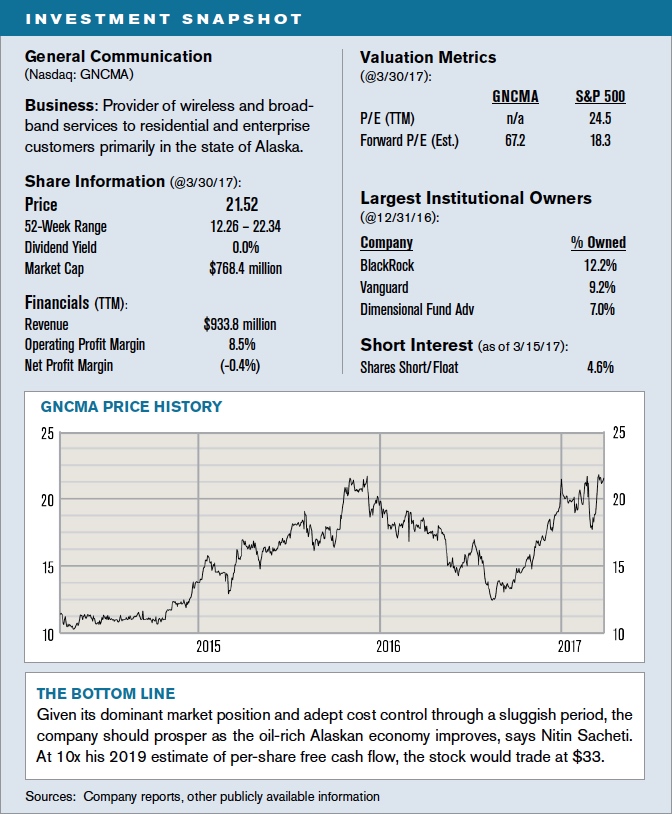

Papyrus Capital’s Sacheti believes the company has made the right financial moves in response to the sluggish Alaskan economic environment. It sold tower assets in mid-2016 for $90 million at an attractive cap rate and reinvested the proceeds into its fiber/microwave network that stretches from Anchorage to Kotzebue. It cut capital spending by one-third and implemented a cost-cutting plan to increase operating margins by 500 basis points, to the mid-30s. Finally, it bought back 7% of its shares last year and plans to use the majority of free cash flow at least in the near term to continue buying back stock. All that should increase earnings power as the Alaskan economy improves, says Sacheti, fueled both by already-recovering oil prices and a large North Slope oil discovery announced earlier this month by Spain's Repsol and U.S.-based Armstrong Energy. That find alone could boost the state’s oil production by some 20%.

Assuming 1% or less annual revenue growth, he believes GCI can earn $3.33 per share in free cash flow in 2019, on which he believes a 10x multiple would be reasonable given the strength of the company’s market position. That yields a price target for the stock of $33, more than 50% above the current price. In a buyout by a Lower-48 competitor – which he isn't counting on – the premium would likely be even higher.